-

Popular search:

When Shall Online Sellers of Goods or Services Apply for Taxation Registration?

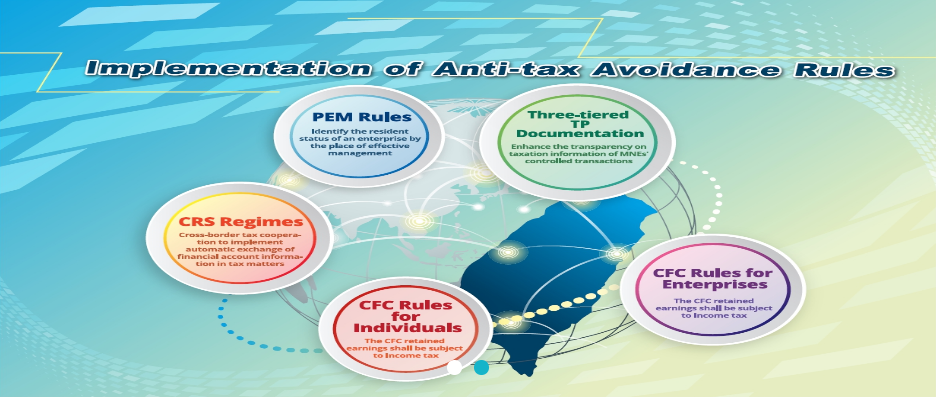

The Nantou Branch, National Taxation Bureau of the Central Area, Ministry of Finance stated that ind... 2025-07-10Exemption Threshold of Accrued Income from Controlled Foreign Company for Profit-Seeking Enterprises.

The National Taxation Bureau of the Central Area, Ministry of Finance expressed that to prevent any ... 2025-07-10Summary of Exports and Imports for June 2025

For June 2025, total exports expanded 33.7% year on year to US$ 53.32 billion; total imports rose by... 2025-07-08Taxpayers who Plan to Dispose of Their Assets Before Paying Additional Assessed Taxes May Face Provisional Injunction of Assets

The National Taxation Bureau of the Northern Area (NTBNA), MOF, stated that in order to effectively ... 2025-07-07The information on the certificate of sales return, purchase return, or allowances on purchased merchandise shall be truthfully uploaded by the seller business entity within a specified time limit.

The National Taxation Bureau of the Northern Area, Ministry of Finance (NTBNA) stated that, starting... 2025-07-07