-

Popular search:

Change in Calculation Method for the Collection Period in Cases with Deferred Execution During Administrative Remedies

The National Taxation Bureau of the Northern Area, Ministry of Finance, announced that effective Jun... 2026-05-29When reporting deductions for losses from the preceding ten years, it should be noted that investment income in the loss year must first be applied to offset such losses.

The Taxation Bureau of the Northern Area, Ministry of Finance (NTBNA, MOF), stated that, as stipulat... 2026-05-29For itemized deductions of medical and maternity expenses in Individual Income Tax, the portion covered by insurance payments should be subtracted by the taxpayer when filing.

National Taxation Bureau of the Northern Area (NTBNA), Ministry of Finance, indicated that when taxp... 2026-05-29FTZ Enterprises Urged to Report Entry, Storage of Goods Accurately to Avoid Penalties

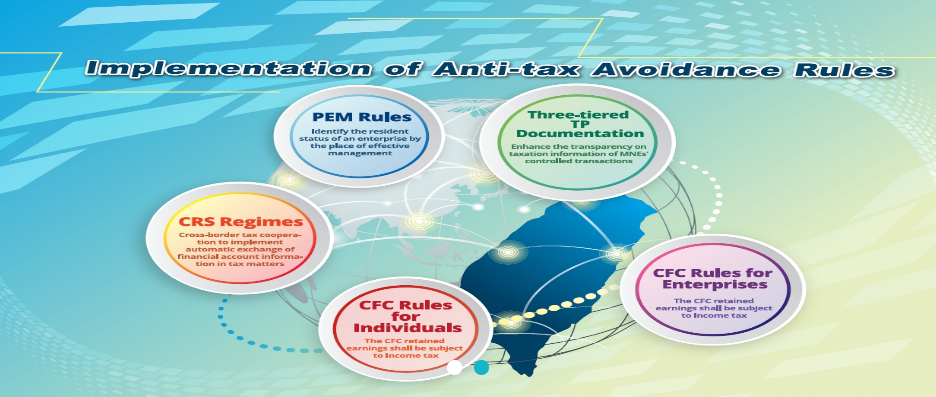

Kaohsiung Customs (KHC) stated that there have been recent cases where Free Trade Zone (hereinafter ... 2026-05-29Profit-seeking enterprises reporting CFC's losses must provide the CFC's financial statements within the income tax filing deadline to be eligible for deduction of assessed losses incurred in the preceding 10 years

The National Taxation Bureau of Taipei, Ministry of Finance, stated that the Controlled Foreign Corp... 2026-05-292025 Individual Income Tax Return

File taxes online-Fast,easy,and accurate,every time